Medical Plans

Medical plans provide employees and eligible dependents with comprehensive coverage for doctor visits, hospitalization, preventive care, and other essential health services.

Medical plans are offered through ASCIP (Alliance of Schools for Cooperative Insurance Programs)

Frequently Asked Questions

Deductible - the amount you pay each year before your plan starts to pay.

Copay - a flat fee you pay for covered services like doctor visits.

Coinsurance - your share of health plan costs (a percentage of total costs) after meeting your deductible.

Out-of-Pocket Maximum - the most you have to pay out-of-pocket each year for health care services. once this amount is reached, insurance will pick up 100% of any subsequent qualifying expenses.

Premium - The amount you pay to belong to a health plan.

In Network - Providers who have agreed to render services at a negotiated rate

Out of Network - Providers who have not agreed to provide services at the negotiated rate. Members can still see these providers, but may experience higher fees, balance billing for the difference between the charged fee and the negotiated rate as well as different deductible out of pocket maximum.

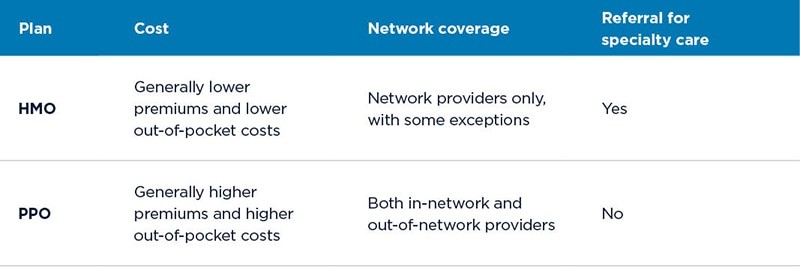

An HMO is a defined network of health care providers that contracts with a health plan to provide care at preapproved rates. Your personal doctor manages your care and refers you to specialists in the network.

In most cases, you’ll need a referral from a personal doctor to get specialty care. But certain specialty services — like ob-gyn and optometry — may be available without a referral.

- Lower monthly premiums (the amount you pay each month for coverage)

- Lower deductibles, or no deductibles (the amount you need to pay before your plan starts contributing to your medical bills)

- Lower payments for covered services

Remember: If you get nonemergency care from an out-of-network provider, you’ll pay the full cost.

How do PPO plans work?

With a PPO plan, you can see any doctor you want — inside or outside the network.

Your PPO plan will have a network of preferred providers. It will probably cost you

less money to see them. But you still have the option to see doctors outside that group.

Do PPO plans require referrals?

No. You can get specialty care without a referral from a personal doctor — from both

in-network and out-of-network providers.

The costs of a PPO plan

PPO plans often have higher monthly premiums and out-of-pocket costs than HMO plans. You may also need to pay a deductible before your benefits begin. If you see

an out-of-network doctor, you’ll usually have to pay the full cost of your visit and

then file a claim to get money back from your plan.

Which is better — an HMO or a PPO?

It depends on what’s important to you. The best health plan is the one that meets

your needs. If you like lower costs and think coordinated care makes things easier, an

HMO plan might be a good choice. If you want to continue seeing a doctor or specialist

who isn’t in a plan’s HMO network, think about a PPO plan.

Advantages and disadvantages of HMO plans

- You pay lower monthly premiums and usually lower out-of-pocket costs,

including prescriptions. - When you get care in the network, you have fewer claims to file.

- Your personal doctor coordinates your care. This can make it easier to take care of your health.

Disadvantages

- HMO plans require you to stay inside their network for care, unless it’s a medical

emergency. - If your current doctor isn’t part of the HMO’s network, you’ll need to choose a new personal doctor.

Advantages and disadvantages of PPO plans

Advantages

- You can see providers both inside and outside the network.

- You can visit specialists without a referral, including specialists outside the network.

Disadvantages

- You typically pay higher monthly premiums and costs for care than with HMO plans.

- You have more responsibility for managing and coordinating your care.

What to consider when choosing a health plan

Before choosing a plan, think about your health care and budget needs. Do you want

a personal doctor to coordinate your care? Do you want lower out-of-pocket costs and

fewer claims? Do you need health insurance for young adults? Are there specific wellness perks you want included? Once you know the answers to questions

like these, you can review the information above and start making your decision.

Health plans have a group of contracted doctors and facilities that they negotiated their rates with — this is their network. If your health plan covers services from providers that aren’t in the network, you may have to pay more to see those providers. Getting care from a network provider can save you money. That’s why it’s important to understand the difference between in-network vs. out-of-network care.

In-network care

A doctor, health care professional, or facility that’s in network has a contract with your plan. Your plan decides to pay a specific amount for a service, and the provider agrees to accept that rate. Depending on your coverage, you might pay none or part of that cost yourself, plus your copay, coinsurance, or deductible. These are your out-of-pocket costs.

Out-of-network care

An out-of-network doctor or facility doesn’t have a contract with your plan. Getting care out of network could cost you more than in network because the rate isn’t negotiated beforehand. The provider decides how much to charge for a service, and your plan may not cover the entire cost. You’ll likely pay the difference, as well as your out-of-pocket costs — your coinsurance or deductible. (Out-of-network care doesn’t usually include a copay.)

Most plans don’t cover any care outside of their network unless it’s for an emergency. In that case, you could be responsible for the entire cost of any out-of-network care you get. To be safe, confirm your care will be covered before you go.

- You change plans and need to find a new primary care doctor.

- Your primary care doctor recommends you see a specialist.

- You move to a different town and want a new doctor closer to home.

- You want to see a mental health or substance use disorder professional.

- Your doctor orders a lab test, X-ray, or treatment that’s not available at their office.

- You need to visit an urgent care and you’re not sure where to go.

When you have an emergency, you usually don’t need to worry about your care being

out of network. Health plans generally consider emergency care to be in network.

What type of care can I get?

Whether you can choose between an in-network or out-of-network doctor depends on what type of plan you have. The most common types are known as HMOs and PPOs.

- Health maintenance organization (HMO) plans — Only in-network care is covered. Your primary care doctor will refer you to most specialty care. HMO

plans often have lower monthly costs. - Preferred provider organization (PPO) plans — Both in-network and out-of-network care are covered, but at different rates. You can see a specialist without

a referral. PPO plans offer more choice and flexibility, usually at a higher monthly

cost.

If you have a plan that covers out-of-network care, there are a few reasons you might choose to get care that way, even if the out-of-pocket costs are higher. For example:

- You need to get care in an area where no in-network options are available.

- Your doctor has left your network, but you still want to see them.

- You need to see a type of specialist that isn’t available in your network.

How do I find doctors in my network?

There are a few ways to make sure a doctor or facility is in your plan’s network.

Your plan likely has an online directory where you can search for doctors, specialists, hospitals, pharmacies, labs, and other clinicians that are in your network. If you need help, call the number on your ID card.

You can also contact the doctor’s office or facility and confirm whether they’re in your plan’s network.

Kaiser Permanente has been providing high-quality health care and coverage for more than 75 years. By connecting care with coverage, we initiated a history of innovation and a new model for health care, where everything is designed to work together to help our members live healthy lives. Our care model enables our teams to think and work as one, coordinating your care seamlessly, so you don’t have to — and delivering better care when it matters most...

You may seeSISCon many of the plan documents. ASCIP partners with SISC (Self Insured School of California) to administer its billing and eligibility functions for Anthem and Blue Shield HMO and PPO plans. This partnership ensures that ASCIP districts benefit from the negotiating leverage of the larger SISC pool while still having access to the local support and unique programs offered through ASCIP.

Benefits are effective on the first of the month following your date of hire, or first of the month following change in status from part-time to full-time

Once hired, you will receive an email from the Employee Benefit Office with enrollment details. Our online benefit system provider American Fidelity will contact you via your district email address to schedule an online enrollment appointment. The system you will have access to during your appointment is called AFenroll which will provide all the employee insurance plans available for you to select from.

Eligible dependents include:

- Legal spouse or domestic partner

- Dependent children under 26 years of age

- Your unmarried children who are deemed disabled by their physician and approved by your insurance carrier.

Eligible children include:

- Your natural and adopted children

- Stepchildren, if you are married to your stepchildren's parent. If you and your spouse divorce, your former dependent stepchildren are no longer eligible for coverage

- Children of your domestic partner. If you and your domestic partner separate, the children of your former domestic partner are no longer eligible for coverage

- Children for whom you have permanent legal guardianship issued by a court of law

- Your children or stepchildren who must be covered under a Qualified Medical Child Support Order

Please note you will be required to provide documentation of your dependent's eligibility

by submitting marriage and/or birth certificates, legal documents for custody or adoption,

the Social Security and medical provider's determination of disability for an

adult child, the first page of your most recent Federal Tax form for spouse verification.

ID cards are mailed at the end of the month prior to your effective date or within 2 weeks after enrollment.

Call the Employee Benefits Office at 714-480-7567.

You will receive a Benefit Confirmation Statement at time of initial enrollment. A copy is also available during Open Enrollment by accessing the online employee benefit portal called AFenroll. Please contact the Employee Benefits Office if you require a copy mid-year.

In general, you may only make changes to your benefits once a year during Open Enrollment

period in October for an effective date of January 1 of the following year.

However, the plan does allow for changes during the year if you experience a "family

status change" as defined by the IRS. Examples of a family status change include:

- Marriage or divorce

- Birth, adoption, or death

- Change in your spouse or domestic partner's employment that would affect

coverage, such as gain or loss of coverage - Change in court order for custody or visitation, or requirement to provide health

insurance coverage - If you have an eligible qualifying event, a request for change must be made within 30-days of the event; otherwise, you must wait until the next open enrollment period.

You will need to bring the following proof that your dependent is eligible and proof of the life event change to the Benefits office before the change goes into effect.

- Marriage license

- Birth Certificate

- Court adoption papers

- Registration of domestic partnership

- Income tax returns

- Employer documentation of loss of coverage

Additional ID cards are available by contacting the insurance carrier directly.

Medical Plan Options

Kaiser HMO Plan

The Kaiser Permanente HMO plan is available to all benefit eligible employees.

Kaiser Permanente owns its own facilities and employs its own physicians. Kaiser Permanente healthcare providers exclusively care for and serve Kaiser members.

With your Kaiser Permanente HMO plan, you get a wide range of care and support to help you stay healthy. Your care team works with you to give you the care you need when you need it, and you get plenty of resources to stay in control of your plan and health.

-

Website: www.kp.org

-

Member Services (800) 464-4000

Retirees Over 65 With Medicare Parts A & B

2 Columns

ClassPass

ClassPassFitness industry leader ClassPass makes it easier for you to work out from anywhere. ClassPass partners with 40,000 gyms and studios around the world, offering a range of classes including yoga, dance, cardio, boxing, Pilates, boot camp, and more. With this ClassPass offer, Kaiser Permanente members can get:

-

Unlimited on-demand video workouts at no cost

-

Reduced rates on in-person fitness classes

As of January 1, 2022, the ClassPass offer for Kaiser Permanente only includes fitness and workouts.

ClassPass is not available to Medi-Cal and Medicaid members.

Active & Fit Direct

With the ChooseHealthy® program*, you also have access to contracted fitness centers in the Active&Fit Direct network. Get access to more than 11,000 gyms with one membership. When Kaiser Permanente members sign up for an Active&Fit Direct gym membership, they can visit any of the 11,000 participating fitness centers in the nationwide Active&Fit Direct network. Participating gyms may include Gold’s Gym, Curves, Anytime Fitness, and more.

The Active&Fit Direct program is available to all Commercial members. It is also available to select Medicare Advantage Plus members. To confirm eligibility, please call Member Services at 800-443-0815. The Active&Fit Direct program is not available at this time to Medicaid members.

Sign in below to access this special Active&Fit Direct rate.

*The ChooseHealthy program is provided by ChooseHealthy, Inc. The Active&Fit Direct program are provided by American Specialty Health Fitness Inc., (ASH Fitness). ChooseHealthy, Inc., and ASH Fitness are subsidiaries of American Specialty Health, Inc. (ASH). Active&Fit Direct and ChooseHealthy are trademarks of ASH and used with permission herein.

ChooseHealthy

Kaiser Permanente members can get reduced rates on a variety of fitness, health, and wellness products through the ChooseHealthy program. This includes:

-

Activity trackers — Save on activity trackers from brands such as Fitbit, Garmin, and more.

-

Workout apparel — Save on clothing and accessories from brands like Sketchers, 2XU, PRO Compression, and more.

-

Exercise equipment — Save on equipment from brands such as TRX, Gaiam, BOSU, and more.

The ChooseHealthy program is not available at this time to Medicaid members.

Sign in below to access this special ChooseHealthy rate.